Why Do Growth Stocks Outperform Value Stocks?

Why Do Growth Stocks Outperform Value Stocks?

Taking a look at growth's recent strong performance.

Not financial advice, meant purely for entertainment purposes. Do your own research before making any investment decisions.

A Debate as Old as Investing

Stocks are often separated into two categories: value and growth. Value stocks are companies with fundamental characteristics that are lower than some baseline, such as the stock market PE (Price/Earnings) ratio or industry PE ratio. Growth stocks are companies who are expected to increase their earnings at a faster rate than the market as a whole or others in their industry. For years value stocks were seen as the vehicle to outperform the market, as it was believed these companies would at some point return to a fair valuation, allowing holders of the stock to cash in on the upwards move. This has been challenged in recent years, notably since the Great Financial Crisis, with growth having significantly outperformed value:

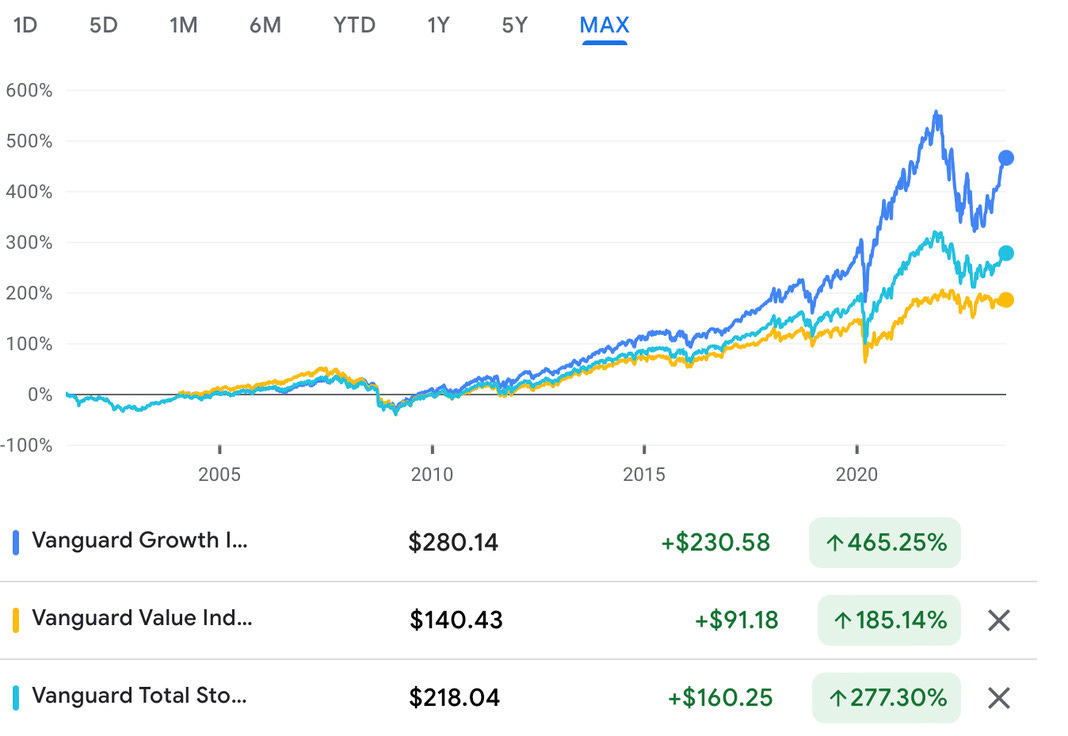

As you can see, the Vanguard Growth ETF has significantly outperformed the Vanguard Value ETF since inception in 2004, with a notable separation post-GFC in 2010. To better show the significance of this outperformance, the chart below shows these same two funds compared to the Vanguard Total Stock Market ETF, VTI:

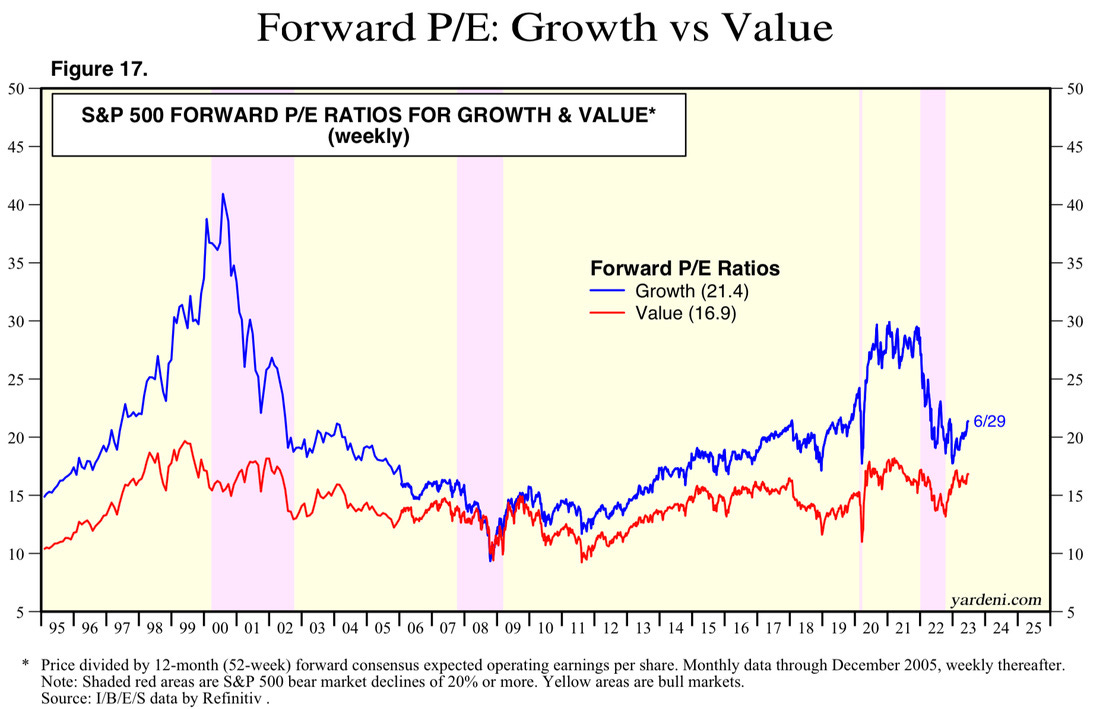

A near perfect image of these price return charts is the forward price-to-earnings (PE) chart shown below. While this chart goes back further than what is shown above, we see the valuations of growth and value in relative lock-step, with growth trading at slightly higher valuations, until growth valuations broke away in growth post-2020. This same occurrence can be seen in the stock chart above.

The goal of this article is to examine why growth has seen staggering outperformance over value in recent years, and determine if this recent trend is ready to change. We will start by discussing why investors would choose growth over value and vice versa.

Growth or Value?

“All investment is value investment, in the sense that you're always trying to get better prospects than you're paying for.” - Charlie Munger

Well that settles it, there is no such thing as growth investing, and it was all value investing after all. In all seriousness, there are distinctions between growth and value investing, but what they do have in common is the belief that what you are buying will be worth more in the future.

Growth investing aims to increase an investor’s capital through buying companies that growing faster than others in their sector or the economy as a whole. These companies generally don’t pay dividends, instead using their earnings to invest in the business. These “growth stocks” often trade at premium valuations due to their perceived growth prospects. Investors are willing to pay more today for tomorrow’s earnings, as they are expected to grow rapidly. In taking a look at Vanguard’s Growth ETF, VUG, you can get an idea of what types of companies are growth companies: Apple, Microsoft, Amazon, Alphabet, Tesla, Nvidia, Visa, and Mastercard, among many others. These companies are growth quicker than their peers, and trade at high valuations.

Value investing, on the other hands, is a strategy that looks to buy stocks when they are “underpriced” or “undervalued” by some metric. Value investors often look for stocks the market has left behind, forgotten about, and has potential to rebound due to this misvaluation. Value investing is what has made Warren Buffett a wildly successful investor over his lifetime, using the principles of value investing in Berkshire Hathaway. In looking at Vanguard’s Value ETF, VTV, you can get an idea of what types of companies are value stocks: Berkshire Hathaway, UnitedHealth, Exxon Mobil, Johnson & Johnson, JPMorgan Chase, Broadcom, and Procter & Gamble, among many others. Often, value stocks are low PE (but not always), slower growth, and more mature companies. Value stocks also often pay out healthy, stable, and growing dividends, making value investing more suitable for older investors who may want income.

Why Has Growth Outperformed Value Since 2010?

“In fact, the period from mid 2007 to late 2020 was an anomaly in an otherwise long history of Value dominance. In those 13 years, Value underperformed universally across geographies, sectors, metrics, and asset classes” - JPMorgan Asset Management

Revisiting this chart from earlier, which shows Vanguard’s Growth and Value indices since inception, we can see that since roughly 2010 growth has been crushing value’s performance. Why is this? The Great Financial Crisis crushed economic growth worldwide, forcing central banks to lower interest rates to zero to spur economic growth. These massive quantitative easing programs flooded the market with money, which was a massive boost to growth stocks. This allowed many growth companies to fund risky ventures with nearly free cash, and allowed companies to take on losses as they grew their business, all in the name of growth and future profitability. More than ever did investors become obsessed with the story of companies—looking at growth in users, products sold, or some other metric of growth—instead of profitability. Companies did not need to be profitable today, as the faucet of free money would not be running dry any time soon, so all they had to worry about was growing.

This is not the same story for value stocks, however. Most companies considered value stocks are more mature, slower growth companies. They are stable, and often grow as long as the overall economy is growing. While these businesses were stronger than ever, the stocks underperformed. Why buy Procter & Gamble when you can buy Amazon or Alphabet instead? Even during the 2022 bear market, while value stocks did not see price declines as significant as many growth companies did, if you have held growth over value for any time longer than 2 years you still did better than value investors. Even now as the Federal Reserve raises rates, an environment where value often outperforms, growth stocks are crushing value. Why is that?

Bigger and Better Than Ever

There is a strong argument to be made that some of the largest growth companies in the world are bigger and better than ever, and consumers will still want their products and services even as budgets tighten. This has led to Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla absolutely crushing the stock market this year. In fact, for most of this year, these seven stocks accounted for the entire gain of the S&P 500. Part of this is due to the craze in AI, but many also believe these stocks were oversold in 2022. People have become accustomed to buying the biggest and best tech companies, which are all often considered growth companies, and really have not been given a reason to do so.

While value did well in 2022, its performance is dwarfed by what tech has done this year. Many even argue that value is overvalued, and is due for a massive pullback. Let’s take Coca-Cola, which is trading at a PE ratio of 26. Coca-Cola’s PE ratio has been increasing since 2011, post-GFC. If it is supposed to be a value stock, why does it trade at such a high PE?

There are two components to why a company trades at a particular PE Ratio: growth and risk. If a company is expected to grow at a high rate in the next 5 years, it is likely it will trade at a high PE, especially if that growth is faster than the industry. On the other hand, a slow growing company that is perceived to be less risky, like a Coca-Cola, will also trade at a higher PE ratio because of this perceived safety. Nvidia, on the other hand, now trades at an extraordinarily high PE due to the growth in artificial intelligence, and the demand for their chips. Neither one is wrong for trading at high PEs—it is up to you, the investor, to determine what you want to pay for when buying a stock, and many have been choosing growth over stability.

So, Why has Growth Outperformed Value?

Since the Great Financial Crisis investors have wanted to own companies that grow faster than GDP. This, combined with near-zero interest rates, has made growth a much more viable investment. For most of history value had outperformed growth, a truth which Warren Buffett and many other value investors proved. However, it is fair to say we have entered an era in the stock market where the promise of potential future earnings carries more value than a track record of reliable earnings. The promise of future profits is often more exciting for people to get behind,—a new innovative tech company that promises to grow at 50% per year is much more exciting than selling toilet paper or soft drinks.

As interest rates are promised to be “higher for longer” time will tell if value will make a roaring comeback. As of now this doesn’t seem to be the case, as leadership this year consists of only the largest growth companies. Such a short period does not make a trend, but stocks currently do not care about interest rates. If this sentiment changes, however, it is likely companies that make the products and offer the services of every day life: Procter & Gamble, Coca-Cola, Pepsico, Chevron, and many others, will begin to outperform. Of course this is just speculation, but the only trend that has stood the test of time in the stock market is that stocks move up and to the right over time.

Sources:

JP Morgan Asset Management . Source.

Yardeni Market Valuations. Source.

How Interest Rates Affect Stock Market. Investopedia. Source.

Stock Tickers Mentioned:

VUG 0.00%↑ VTV 0.00%↑ VTI 0.00%↑ AAPL 0.00%↑ AMZN 0.00%↑ GOOG 0.00%↑ GOOGL 0.00%↑ NVDA 0.00%↑ TSLA 0.00%↑ META 0.00%↑ MSFT 0.00%↑ KO 0.00%↑ PG 0.00%↑ JNJ 0.00%↑ XOM 0.00%↑ UNH 0.00%↑ JPM 0.00%↑ AVGO 0.00%↑ PEP 0.00%↑ CVX 0.00%↑