Waste Management is the Future of Sustainable and Renewable Energy.

Waste Management is the Future of Sustainable and Renewable Energy.

WM does a lot more than just pick up your trash every week.

If you aren’t already, be sure to subscribe to have every edition of The Simple Stock Report sent straight to your inbox! Every free subscription is greatly appreciated!

WM, formerly called Waste Management (I’ll use them interchangeably), is often considered a trash company. I don’t think this is fair, because they are also a recycling and renewable energy company. In all seriousness, WM does a lot more than pick up your garbage every week, and you may not even realize it. For example, WM uses the methane gas produced from its landfills as renewable energy in the form of electricity, along with using this natural gas as fuel for its fleet of trucks.

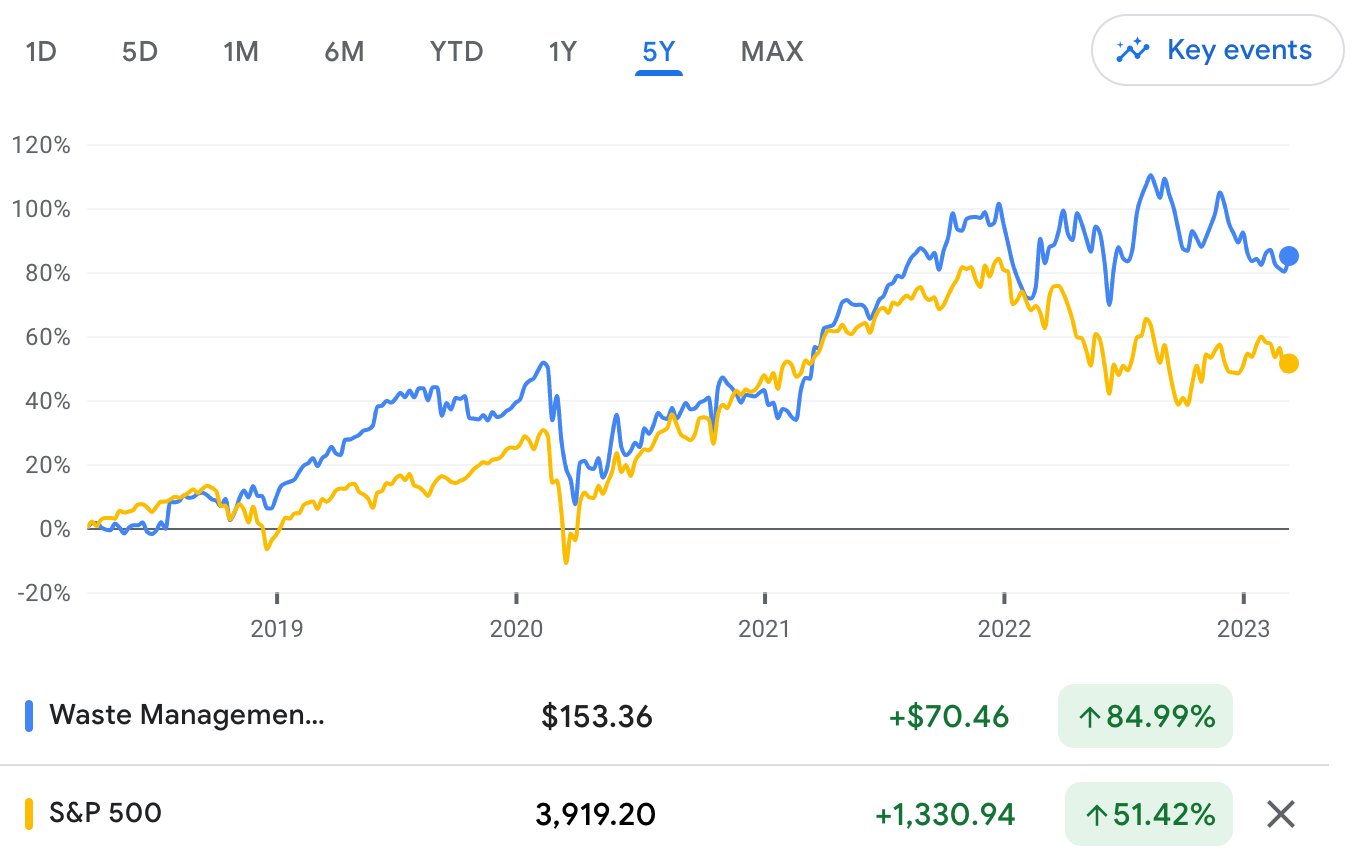

WM 0.00%↑ recently raised their quarterly dividend 7.7% per share to $0.70, the 20th consecutive year they have raised their dividend. Let’s take a look at the business of WM that allows them to consistently raise their dividend and outperform the benchmark S&P 500 Index

WM is a leader in recycling, waste management, and renewable energy.

Investments in their sustainability businesses show less liquidity than is actually available at WM.

WM does a lot more than pick up your trash.

The Basics

WM describes themselves as North America’s leading provider of comprehensive environmental solutions, providing services throughout the United States and Canada. They partner with residential, commercial, industrial, and municipal customers and the communities they serve to manage and reduce waste at each stage from collection to disposal, while recovering value resources and creating clean, renewable energy.

WM’s “Solid Waste” business is operated and managed locally by their subsidiaries that focus on distinct geographic areas and provide collection, transfer, disposal, and recycling and resource recovery services.

The WM Renewable Energy business is a leading developer, operator, and owner of landfill gas-to-energy facilities in the U.S. and Canada that produces renewable electricity and renewable natural gas, which is a significant source of fuel for their fleet of natural gas powered trucks.

WM owns or operates 259 landfill sites, the largest network of sites in the U.S. and Canada. They also manage 337 transfer stations that consolidate and transport waste efficiently and economically. They also use this waste to create energy, recovering the gas produced naturally as waste decomposes in landfills and using the gas in generators to make electricity. WM is also a leading recycler in North America, handling materials such as cardboard, paper, glass, plastic, and metal.

It is also important to note that WM’s largest customer represents less than 5% of annual revenue in 2022. Operating revenues are generally higher in summer months, with this trend being attributed to higher construction and demolition waste volumes. The effects of this are felt in the 2nd and 3rd quarters.

WM Renewable Energy

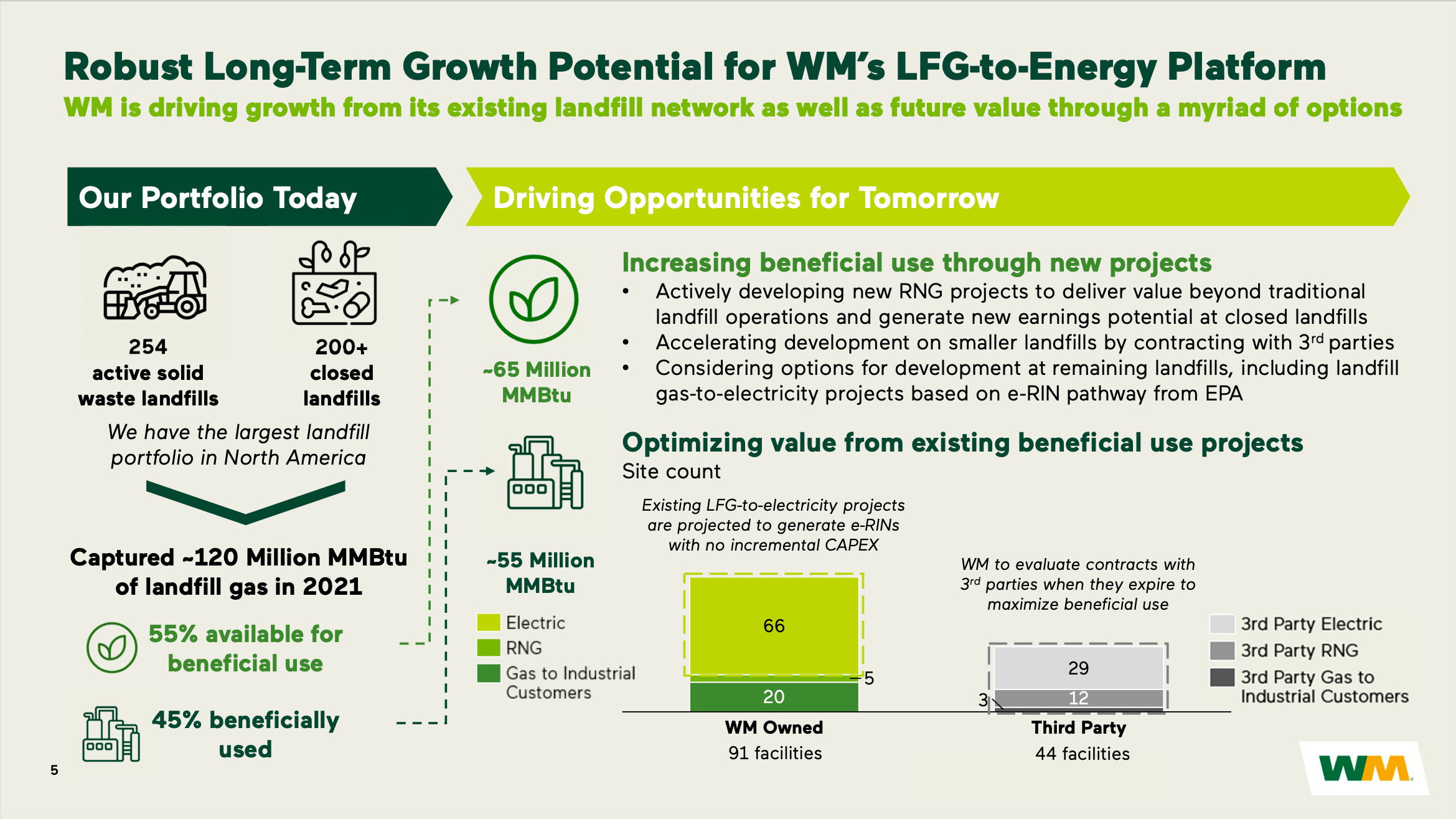

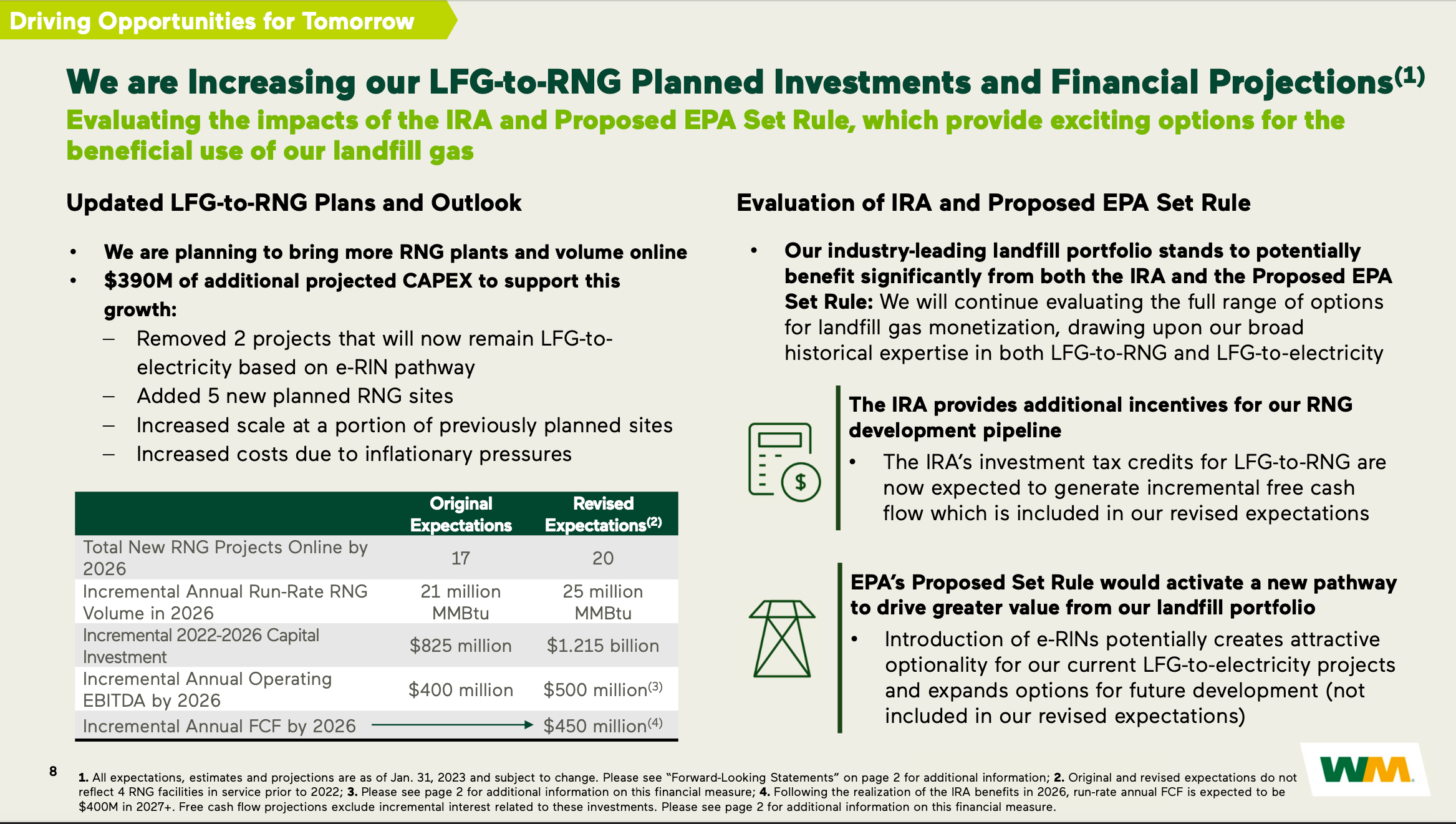

While their “Solid Waste” business is important to WM, I want to focus on the part of the business that I believe will be critical moving forward: Renewable Energy. As of year-end 2022, WM had 135 “landfill gas beneficial use projects” producing commercial quantities of methane gas at owned or operated landfills. 95 of these projects use the processed gas to produce electricity, which is sold to public utilities or power cooperatives. At 23 of these projects the gas is delivered by pipeline to industrial partners as a replacement to fossil fuels. For 17 of these projects, the gas is processed to pipeline-quality gas and sold to natural gas suppliers.

WM has been making significant investments in their Renewable Energy business, recognizing this will be a key driver of growth for years to come. Below are slides from a recent investor presentation where WM discusses their growth in their Renewable Energy segment:

With environmental groups and governments both pushing for more solutions to reduce fossil fuel usage and increase usage of renewable energy, WM stands at the forefront of this solution. While WM’s clean energy business isn’t as fun as a new EV company, they are going to be the “plumbing” of renewable energy, the source of the energy for many customers.

The Financials

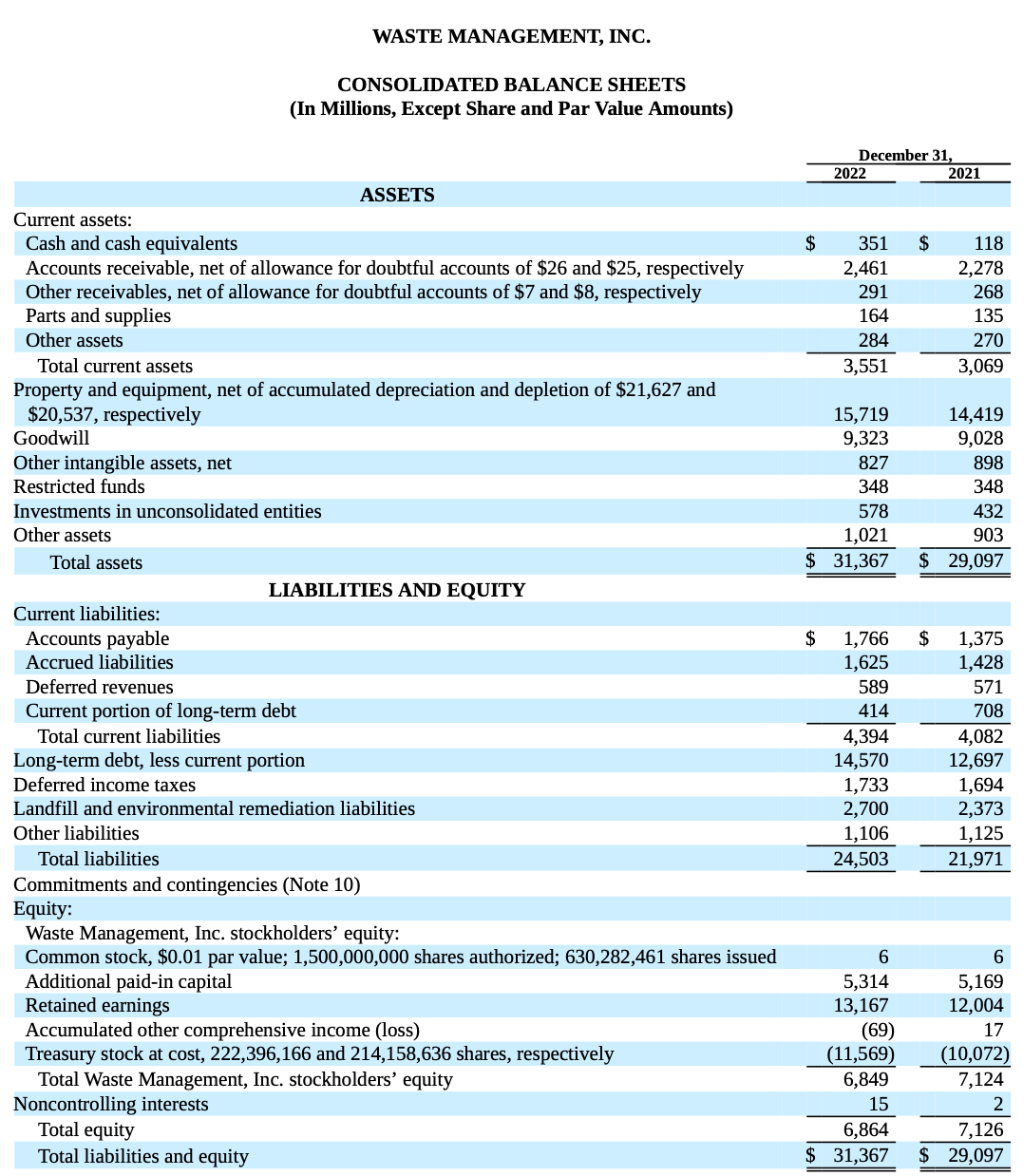

Waste Management finished 2022 with an operating margin of 15.5%. Total operating revenue came in at $19.698 billion, and after all costs and expenses net income totaled $2.238 billion, a margin of 11.4%. For comparison, average operating margin of Environmental and Waste Services segment companies is 13.25%, and average net margin is 7.29%. This puts WM ahead of its competitors in terms of profitability.

Now shifting to the balance sheet, as seen below, we see a rather healthy balance sheet. According to WM’s 4th quarter earnings release, free cash flow without the effect of sustainability growth investments comes in at $2.537 billion for the entire year. This is plenty of cash flow to pay off long term debt, much of which is cheap debt, as it comes due, so there is no serious concern about debt repayments here.

One area of concern you may see is the working capital of WM. Working capital is calculated by subtracting current liabilities from current assets, and ideally you’d like to see a positive amount of working capital. In WM’s case, I am not concerned about this potentially liquidity issue, and for my reasoning we turn back to free cash flow. As I briefly mentioned before, WM is investing heavily into becoming a more sustainable company, along with offering more sustainable products and solutions. This has a short term negative effect on the balance sheet was the benefits from this investments are not yet felt. While it is appropriate to pay attention to WM’s liquidity, the “issue” should resolve itself in the coming years.

I think it is also important to point out the current debt/equity ratio is 0.4, meaning the debt of WM is low risk. A D/E ratio lower than 1 means the company’s equity is larger than its debt, often signaling the debt is low risk.

WM, More than a Trash Company

While Waste Management is known for picking up trash every week, they have expanded their business and made investments in areas that will only become bigger as we move to a cleaner future, such as recycling and renewable energy. This potential to be a leader in renewable energy is likely why WM shares trade at a premium to the market, with a P/E ratio of 29 (market average is 18). You may not have thought of WM as a leader in the green revolution, but they are building the groundwork to lead the fields of recycling and renewable energy for years to come. They are a clear leader in their industry, and I believe they are currently in an investment cycle to widen their moat. I have owned WM for over a year now, and I have no plans of selling this trash company.

Sources: WM Investor Relations: Sustainability Report, 2022 Annual Report, Q4 2022 Earnings Release.

The saying that WM is "a trash company" might not have the same ring as they move towards green energy and sustainable options! I own WM as well and have no plans to sell.

Great write-up!