So, Where is this Recession Everyone is Talking About?

So, Where is this Recession Everyone is Talking About?

What the Bond Market, Stock Market, and Jobs Market tells us.

Be sure to like this post and subscribe to never miss a post like this one!

The bond market is telling us a recession is near as crucial bond yield curves remain inverted.

The stock market is running to start 2023, climbing back from lows in October.

The job market is as strong as ever, but that might not be good news for inflation.

Maybe Everyone is Confused

If you follow any amount of financial news, or read enough of my newsletter, you have heard talk of a recession for the past year, but where is it? While some companies are seeing growth slow in recent quarters, this can be attributed to tough year-over-year comparisons due to the explosion of growth after the end of lockdowns. Even with earnings slowing, the stock market is rallying to start 2023. The job market has recently begun to slow, but unemployment still remains at historic lows. While there is optimism in the job and stock markets, the bond market is telling us a completely different story.

Let’s take a look at the bond market, job market, and stock market individually and see what each are saying about a possible recession in the near future.

What The Bond Market is Telling Us

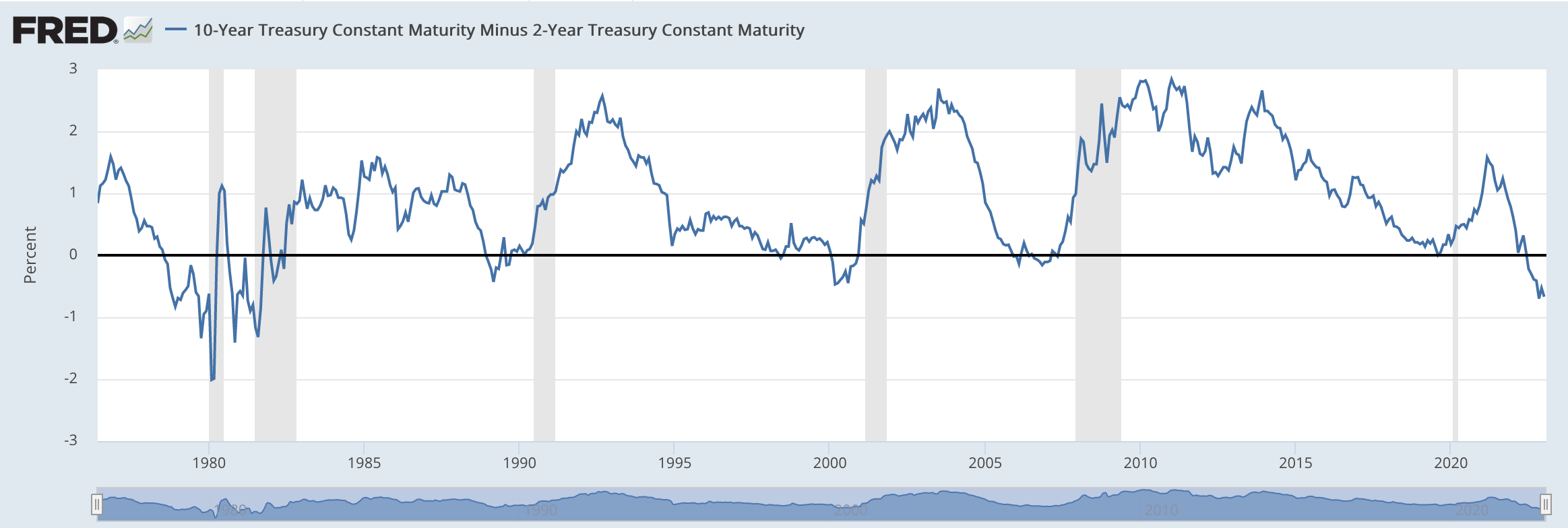

The bond market is a beast that I unfortunately can’t break down in a simple article, but I want to focus on three US bond yields: 10 year, 2 year, and 3 month bonds. When the economy is considered healthy, the 10 year bond should yield higher than the 2 year and 3 month bonds. This makes sense, the incentive to buy longer duration bonds must be that the yield will be higher, rewarding you more than shorter duration bonds. But this is currently not the case:

The first chart above shows the 10-year treasury bond maturity minus the 2-year treasury bond maturity, and the second chart shows the same 10-year treasury bond minus the 3-month treasury bond maturity. I am showing the long term view for both of these graphs because they show the point I want to make very clearly.

As I mentioned before, ideally the 10-year treasury bond has a great maturity than the 2-year or 3-month bonds, but when this is not true it is considered a bond yield inversion. Bond yields rise as prices fall, so the inversion of the yield curve is a sign investors are worried about the short term prospects of the economy and want longer duration bonds. Every single time this has happened, a recession has followed in the next 12 to 18 months. Every. Single. Time. The 10-year/2-year curve inverted in July, and the 10-year/3-month curve inverted in October. Take this as you will.

The Stock Market Doesn’t Care About a Recession

In the past year, averages such as the S&P 500 have come cratering down from all time highs, at one point even entering a bear market, which is a drop of 20%+ from all time highs. Individual stocks, especially stocks in the tech sector, saw their valuations slashed. Many pandemic favorites such as Zoom, Teladoc, and Peloton have fallen so far they may never recover. Yet suddenly, there is a new wind in the markets. With the S&P 500 up nearly 10% in January alone, what changed? Is this move justified, or is it set to fall once again?

Major companies such as Google, Apple, Amazon, and 3M are beginning layoffs, GDP growth is expected to fall to the lowest levels since the Great Recession, and interest rates are approaching 5%. These three factors together would logically strike fear into investors, but this has not been the case. A slowing job market means the Fed is closer to pausing interest rate hikes (but as we will discuss later, it may not be slowing), and possibly even cutting rates, a positive catalyst for the stock market. The consumer is also still spending, which will help GDP continue to grow. While the market is rallying because of these factors, I do believe its attention is misplaced.

The market is looking forward to and expecting rate cuts at the end of 2023. The problem is, economic conditions will have to deteriorate significantly for this to come true. So while the market is expecting that rates will soon be lower, I believe what gets us there needs to be considered. For rates to be cut, ignoring the still high levels of inflation, unemployment would have to spike and the consumer would have to run out of spending power, which would likely put us into a GDP recession. If the consumer loses spending power, then company earnings will fall even further than they have in the recent year, and valuations would have to correct.

Of course it is possible the economy avoids any form of recession, inflation comes down to long term averages, and unemployment never spikes, which would be good reason for the stock market to rally. From the way I see it, however, the stock market may be overlooking how we get to its desired outcome of lower rates.

Jobs, Jobs, Jobs

This is where everything goes off the rails, in my opinion. In the January jobs report, nonfarm payrolls was expected to increase 187,000, but instead came in at an astonishing 517,000. On top of this, unemployment fell to 3.4%, the lowest since 1970. The Federal Reserve needs to see the labor market contract in order for them to have confidence their work is paying off. This is not happening whatsoever.

In the blink of an eye, the stock market went from good news is bad news and bad news is good news to good news is good news and bad news is bad news. While the market initially fell on the strong jobs report, it recovered much of its losses on Friday after the report. We went from cheering bad job reports, as it gave us hope that the Fed could stop raising rates, to cheering good jobs reports, because it means we might avoid a recession.

Below is the Phillips Curve, it proposes that, in the short run, inflation and unemployment have an inverse relationship. Like every other economic idea, this is not perfect, but it tells the story that worries me. How can we reasonably expect inflation to come down to 2% if the job market is still strong and people still have excess savings to spend. The Federal Reserve can talk about a soft landing all they want, but inflation will not break if unemployment remains at historic lows.

So, Where is the Recession?

The bond market is screaming recession, the stock market has changed its mind on a recession, and the job market is as strong as ever. Well if this isn’t confusing then I don’t know what is. Bulls will give you 100 reasons we are going to avoid a recession and see new all time highs, and Bears will give you 100 reasons this recession will be the worst ever and new lows are coming. As usual, I am sure the answer is somewhere in the middle of the two.

Personally, while every piece of data is going against me, I don’t think we will be able to avoid at least a mild recession. Unemployment HAS to increase to get inflation down to the Fed’s 2% target, and I think at some point this year we will see it start to tick up. Spending will slow as rate hikes continue to hit the financial system, which will be reflected in GDP. The good news in my scenario? The stock market typically bottoms before a recession starts, so maybe we have already seen the lows. That being said, only time will tell, and I’ll be here to talk about it.

There is a chance we defy odds. However I think the more we talk about where the recession is, the better chance it has to happen.

Companies and CEOs will assume it’s inevitable and or they would rather not be on the wrong side of it. They will prepare their company for recession and essentially form one.