Mid-Cap Stock Deep Dive #1: Columbia Sportswear

Mid-Cap Stock Deep Dive #1: Columbia Sportswear

A new series uncovering the world of mid-cap stocks.

At the time of writing this, I do NOT own shares of COLM. This article is my opinion, and is not meant to be taken as financial advice.

Untitled Mid-Cap Series

This article is the first in a new series which will cover mid-cap stocks. What exactly is a mid-cap stock? Well, after reading many definitions and seeing that really nobody has a definite answer, I have decided that a mid-cap stock is a company that isn’t too big but isn’t too small. Maybe another good definition is it is a company you’ve heard of but is smaller than you thought. Either way, I thought it was time to research some of the mid-cap names that seem to be forgotten by investors, and maybe find a diamond in the rough.

I’ve been trying to think of a clever name for this new series for quite some time now, so for now I am leaving it untitled. At some point it’ll have a great name, but not yet.

What Inspired Me

A few weeks ago I found myself at a Columbia Sportswear outlet, and as I was getting a great deal on a hoodie I decided I would take a look at Columbia’s financials, as they are a public company (COLM 0.00%↑). What I found was an extraordinary company, by my standards, but one that I am not sure if I want to buy. Let’s take a look.

What Does Columbia Do?

Columbia Sportswear designs, develops, markets, and distributes outdoor, active, and lifestyle products. These products include apparel, footwear, accessories, and equipment. Columbia offers four different brands: Columbia, SOREL, Mountain Hard Wear, and prAna.

Columbia is, obviously, their oldest and most well known brand. This brand covers all categories of products they offer. SOREL is a footwear brand. Mountain Hard Wear is a premium brand, offering apparel, accessories, and equipment meant for mountaineering, climbing, skiing, snowboarding, and camping. PrAna offers apparel, accessories, and equipment for trail, climbing, studio, and water based activities.

They do not own, operate, or manage their manufacturing facilities, instead most of their products are produced by contract manufacturers located outside of the United States. This, according to Columbia’s 10K, “maximizes our flexibility and improves our product pricing”.

Business has similar seasonality trends as compared to the rest of the apparel industry, which includes seasonal weather and discretionary consumer shopping patterns. Sales for Columbia are weighted substantially toward the third and fourth quarters, while their operating costs are evenly distributed throughout the year. In 2022, for example, over 60% of sales and over 75% of operating income were realized in the second half of the year. This seasonality also impacts the balance sheet, with the lowest cash and highest inventory balances usually at the end of Q2, in preparation for their busy season, and highest cash and lowest inventory balance at the end of Q4.

Columbia uses both wholesale distribution channels and DTC (direct-to-consumer) channels to sell their products. Wholesale distribution consists of small and large sporting goods stores, department stores, and online retailers. DTC includes Columbia branded stores, retail outlet stores, and e-commerce sites.

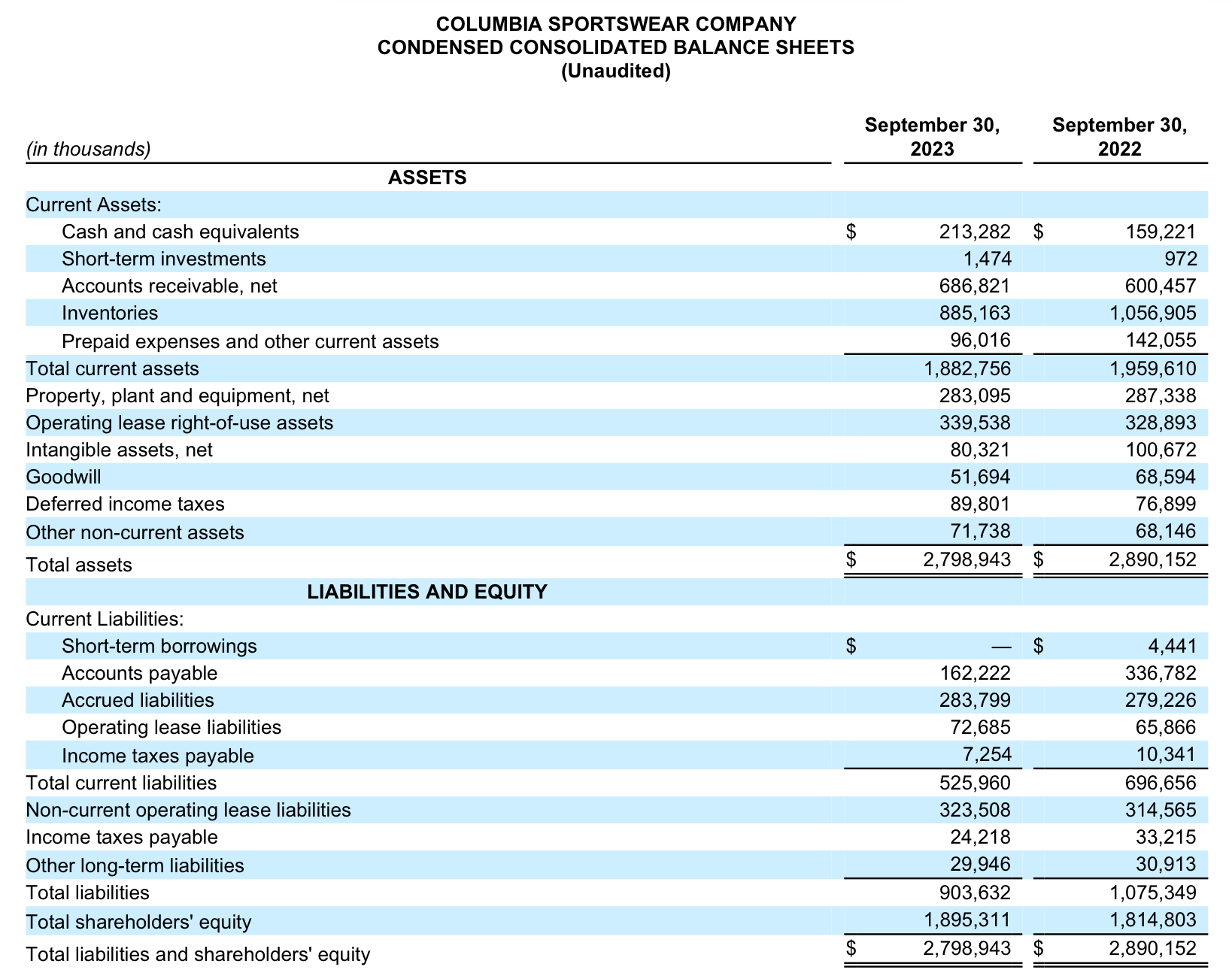

The Balance Sheet

I’ll start off the discussion of Columbia’s financials with my absolute favorite part about this company: the financials. One of my favorite things in a company is either no debt or very cheap debt. In Columbia’s case, they have absolutely zero debt! Sure they have lease and other operating liabilities, but they don’t have any long-term debt to repay. This is great, because it opens up options when cash flow is strong, but doesn’t constrict them when business isn’t going great.

As you can see in the above balance sheet, they have been able to lower their inventory balance as compared to last year, an issue many apparel companies have had to deal with (Nike is a great example). Other than that, as an accounting major, nothing else on this balance sheet jumps at me. It is a healthy and strong balance sheet.

Just for comparison purposes, below is the 2022 year-end balance sheet, just so you can see the effect that the seasonality of Columbia’s business has on their financials:

Again, here you see higher cash balance at year end. Columbia did have inventory issues at the end of 2022, but as you can see they have started to work those off through three quarters of 2023. If you were to check back with Columbia in just one quarter, their balance sheet would look much different than it does at the end of Q3.

Margins and Cash Flows

Margins have compressed for Columbia in the past few years, which could be a cause for concern. Gross margins were 51.5% in 2021, 49.4% in 2022, and 49.2% YTD in 2023. Operating margins were 14.4% in 2021, 11.3% in 2022, and 8.1% YTD in 2023. Net profit margins were 11.3% in 2021, 9% in 2022, and 6.5% YTD in 2023. You can see the obviously concern here, being that margins across the board have compressed in recent years.

The main reason are inventories. Columbia, like many other retailers, has been forced to mark down prices to sell through inventory, which causes pressure to gross margins. Again, this was the same problem Nike has faced for some time now, and is why that stock has struggled the past couple of years. Comparing 2021 and 2022, you see gross margins fell 2.1 percentage points, operating margins fell 3.1 percentage points, and net profit fell 2.3 percentage points. This makes it clear that the loss in gross margin, caused by the inventory problems I discussed, is the main driver of margin compression. This is likely not to continue much longer, and margins should be expected to return to normal. I didn’t compare 2023 to the two previous years, as there was a goodwill impairment that does not make the margins comparable to the year prior.

Cash flows are hard to compare over the past few years due to the changes in inventory and other asset and liability accounts. That being said, changes in inventory account for any negative cash flow seen by Columbia in the past two years. Taking 2021 as an example, free cash flow was just over $300 million, and in 2020 $250 million. 2022 ended at -$75 million and YTD 2023 is at -$22 million. I expect the 2023 figure to improve after Q4 (as does management, offering guidance of just over $400 million free cash flow), and to normalize back to trend for 2024.

It is important to note the challenges facing Columbia can be seen at just about any apparel retailer, but they have handled it well in my opinion. A direct competitor of theirs, VF Corp, is struggling to find its ground as it has been forced to restructure, slash its dividend, and hire new management to right the ship. Columbia has hit turbulent times, but has been able to perform well through them.

Valuation, Performance, and Dividend

COLM is trading at 16.5x earnings, and 16x forward earnings. I would say this is a fair valuation for COLM, trading just below a market valuation. While retail is a tough business, with extreme discounting and a wide array of competition, Columbia is able to hold its own attracting to a niche consumer.

COLM has traded nearly in-line with NKE this year, while VFC has lagged behind them both. VF Corp’s underperformance is an article in itself, but my comments about NKE and COLM seeing the same headwinds hold true in the eyes of the market.

If you’re a fan of dividends, then COLM is nothing short of an interesting story here. They have a current payout ratio of 26%, but haven’t increased their dividend in 2 years, with it stuck at a $1.20 per share payout, giving a yield of 1.55%. It seems to me they have a capacity to increase the dividend, but choose not to out of safety. I guess after watching their competitor VF Corp slash the dividend to bare bones, it might make sense to hold steady and let inventory issues abate. I would expect growth from their dividend in the coming years.

My Final Thoughts

I think Columbia is a great company with a strong balance sheet and great competitive positioning. That being said, I can’t currently bring myself to own COLM stock. Apparel and retail are tough businesses, which require staying on top of trends and using heavy discounting to clear excess inventory. While this business has the ability to see high margins, that requires products to be sold at full price. Very few brands can get away with being full price retailers, with an example being lululemon, and even they are forced to discount products regularly to clear inventory. Maybe one day I’ll change my perspective, or even maybe trade in and out of this stock, but right now I can’t bring myself to buying COLM.