History Tells Us The Unemployment Rate Is About To Skyrocket: Here's Why.

History Tells Us The Unemployment Rate Is About To Skyrocket: Here's Why.

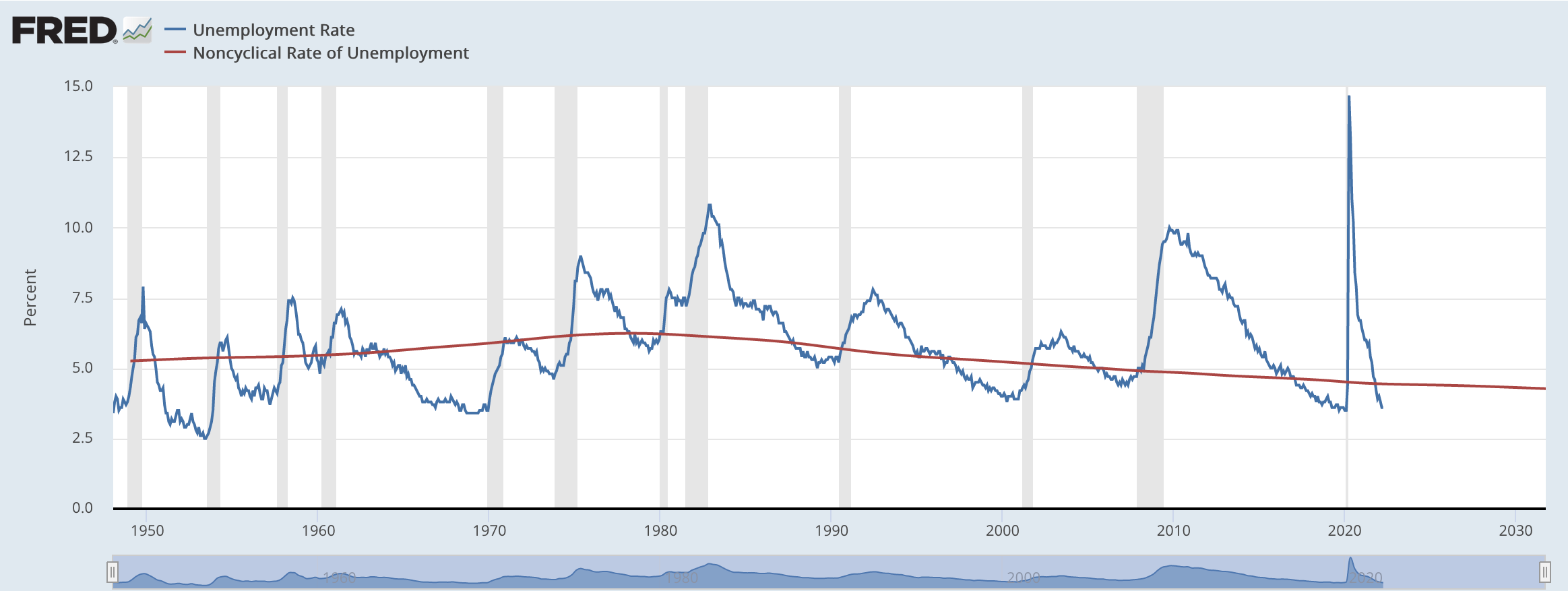

At the time of writing this, the United States unemployment rate is 3.6%. This rate of unemployment is historically lower than expected, under the non-cyclical rate of unemployment of 4.3%. What does this mean? Is this good news or bad news? Let’s dig in.

This chart above is an overlay of the historic unemployment rate vs noncyclical rate of unemployment. The noncyclical rate of unemployment is the noninflationary rate of unemployment, not factoring in aggregate demand (GDP). The closer to this rate (sometimes called natural rate of unemployment), the less turnover in jobs and more stable job growth. When the unemployment rate is higher than the natural rate of unemployment, it is usually a sign of economic strain and more cyclical unemployment, which is unemployment caused by decreased demand. When the unemployment rate is below this line, the economy is usually booming, with high growth and high aggregate demand. By looking at the chart above, you can see that unemployment is cyclical, but why is that?

Since the 1970’s, when the unemployment rate has fallen under the natural rate of unemployment for a significant period of time, it was followed by a jump in unemployment and usually a recession. Before we dig into this trend since the 1970’s, let’s look at why this was not true before then.

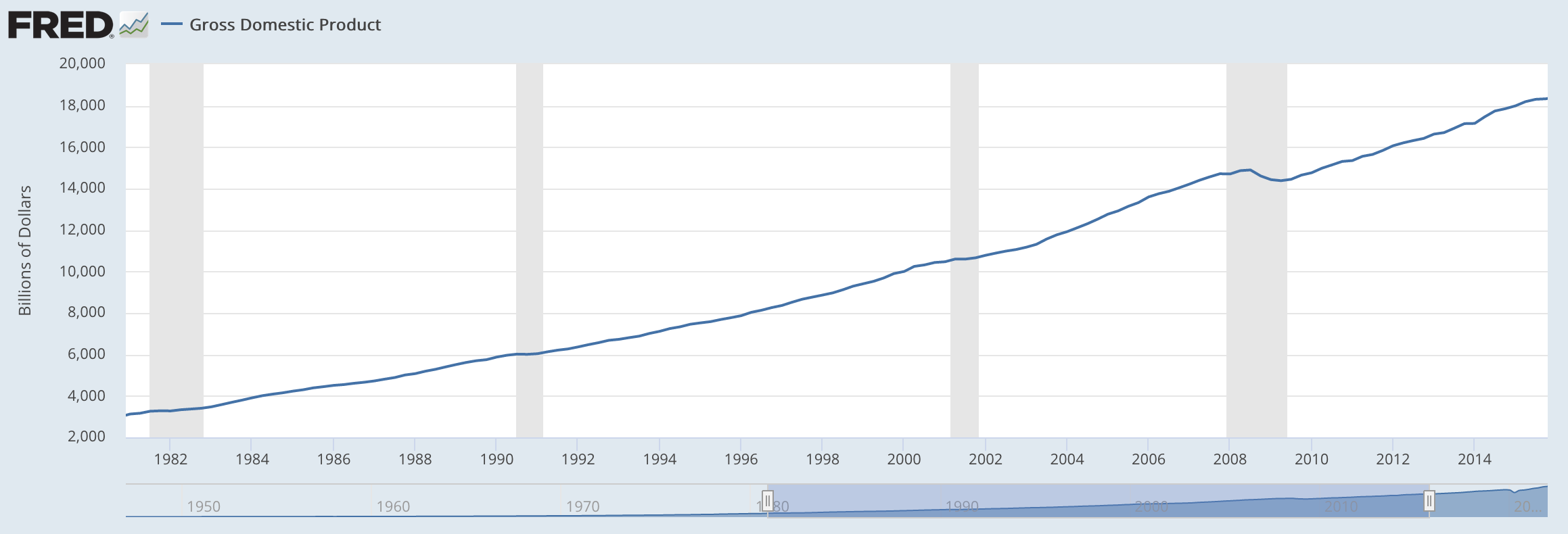

From 1947 to 1981, GDP increased from $243 billion to $3.28 trillion, an over 13x increase.

From 1981 to 2015, GDP increased from $3.28 trillion to $18.3 trillion, roughly a 6x increase in the same time frame.

This is a notable difference, and can be the simple lens we answer the question of “why was unemployment lower before the 1970’s?” Post World War II, the United States economy was the only one left standing. With that along with the GI Bill, which created remarkable opportunities for soldiers returning from the battlefield to get jobs and financial assistance, the US economy could not be stopped during this time. With massive public works projects, such as the construction of the interstate highway system, workers were in high demand, causing long periods of low unemployment. This is a leading contributor to the low unemployment during this time.

Since 1970, 7 recessions were preceded by unemployment falling below the natural rate. It is important to understand that low unemployment does not cause a recession, but instead is a factor that we are able to look at afterwards to see that economic conditions were worsening. This being said, there is a good chance that we will not be able to sustain these low levels of unemployment much longer, and if we did, we would defy much of what history has told us before.

With many top CEOs believing we are heading towards or already in a recession, watching their actions is as important as ever. Companies such as Coinbase, Robinhood, Netflix, Meta, and many others are slowing down and completely stopping hiring, or starting to fire employees, which is a sign that these companies want to cut costs in the short term. These warning signs from top CEOs should not be ignored, and should be used as a sign of caution.

History tells us when unemployment falls below the natural (noncyclical) rate of unemployment, we see a spike in unemployment soon after. Unemployment is a cycle, and we are witnessing the shift from excessive economic growth to slower growth or possible decline. Sustaining low unemployment as long as possible is good for the economy and for employees, but it is not sustainable in the long run. It is likely that as we see confirmations of a recession, unemployment will increase. It is important to remember that unemployment is not a leading indicator, but tells us a lot about how the past could predict the future.

Simply put, the good news is we have seen a very strong economy and strong growth recently in the United States economy. The bad news is that this will correct, and at some point we will see unemployment spike. It is impossible to know the exact time of this, but it will happen fast, and it surely will require the Federal Reserve to change their current course of action.