Everything is Going Procter & Gamble's Way

Everything is Going Procter & Gamble's Way

Margins are expanding, volume growth is returning, and costs are coming down.

At the time of writing this article I own shares in PG. This is not investment advice, and is only meant for entertainment and informational purposes only.

The business of Procter & Gamble is much healthier right now than anyone would have expected two years ago. All segments are growing, margins are expanding, and costs are leveling out. Great brands don’t get traded out of during recessions, and even if consumers traded down it would likely still be within the P&G portfolio.

The above quote was written by me, and posted in my P&G earnings review posted on July 30, 2023. I want you to keep this in mind as we go through the article, because what I said was not the common belief at the time. Going further back into 2022 I was pounding the table on margin expansion and earnings growth for P&G. I refuted numerous analyst downgrades along the way, and it turns out a random college kid got it right and the “professionals” got it wrong. Just something to think about.

The Setup and Schedule Update

First off, there will be no Simple Stock Report on Sunday, February 4th. Regularly scheduled newsletters will resume the 11th with a review of Kenvue’s earnings.

The first half of this article we will go over the overall earnings themselves, segment performance, all mixed in with some management commentary. The second half of this article will be much bigger picture, and how much valuable information this quarter contained. Let’s get started!

The Earnings

Procter & Gamble reported the following for Q2 fiscal 2024:

Net Sales of $21.4 billion, slightly below Wall Street expectations and my own model of $21.8 billion.

Adjusted EPS of $1.84, beating Wall Street expectations of $1.70 and beating my own model of $1.80.

Net Sales grew 3% year-over-year, and 4% on an organic basis (which excludes foreign currency effects along with acquisitions and divestitures). Diluted EPS came in at $1.40, but must be adjusted for a non-cash impairment charge of the carrying-value of some Gillette intangible assets, which is how we get to an adjusted $1.84 (We will touch on this in a moment).

Operating cash flow was $5.1 billion for the quarter, net earnings were $3.5 billion, and $3.3 billion in cash was returned to shareholders through buybacks and dividends.

In December Procter & Gamble announced it would be taking a non-cash impairment charge on intangible assets related to its Gillette business. In non-accounting terms, they believe certain aspects of their Gillette business will earn less money in the future, which means they have to lower the value on their balance sheet. This impairment arose from the weakening of several currencies compared to the US dollar and higher interest rates. P&G also announced it would be restructuring its portfolio in Argentina and Nigeria to address macroeconomic and fiscal issues, which will result in restructuring charges of $1 to $1.5 billion in their next quarter.

Returning to the numbers, margins were strong for P&G this quarter, with gross profit margins increasing 520 basis points to 52.7%, with 240 points lead by productivity increases (more on this later), 200 points of favorable commodity costs, and 190 basis points from increased pricing. Operating and net profit margins are not comparable due to the non-cash impairment charge taken during the quarter.

P&G maintained their net sales guidance of 2-4% for the year. They also maintained organic sales growth in the range of 4-5% for the year. EPS guidance was raised from a range of 6-9% to a range of 8-9% for fiscal 2024. This equates to $6.37 to $6.43 of earnings for fiscal 2024.

Segment Results

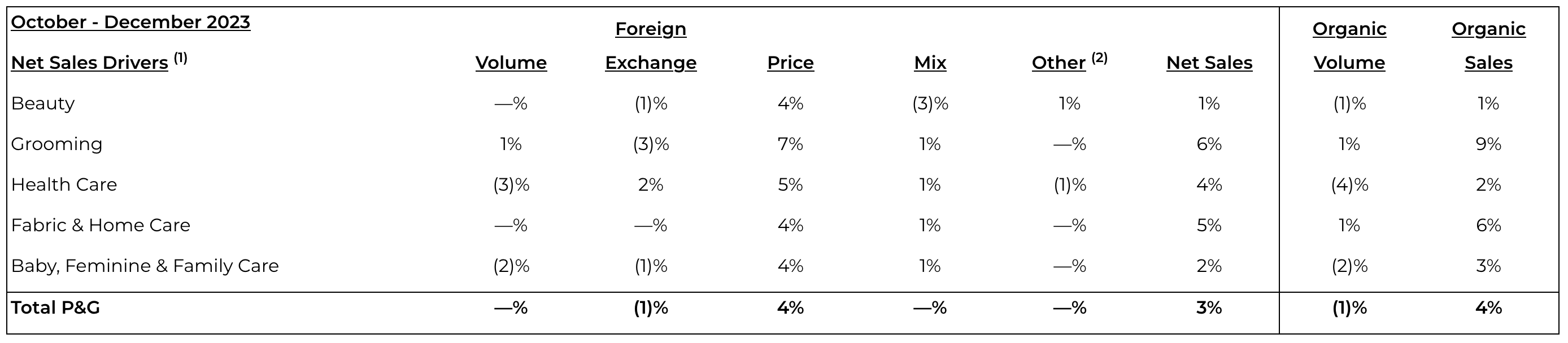

Beauty organic sales increased 1% versus a year ago. Skin and Personal Care declined mid-single digits due to lower sales of SK-II in China, partially offset by higher pricing. Hair Care organic sales increased high single digits led by increased pricing, premium product mix, and volume growth. Head and Shoulders, the largest shampoo brand in the world, has grown 8% fiscal year to date, and has been a strong driver of growth in this category.

Grooming organic sales increased 9% versus a year ago, driven higher by pricing, mix, and volumes. Despite the impairment charge taken on their Gillette business, management had positive things to say on growth in Grooming. They were clear this charge had to be taken because of the regions they do business in, but in their largest markets Grooming is doing great.

Health Care organic sales increased 2% versus a year ago. Oral Care increased mid-single digits due to increased pricing and premium product mix, partially offset by volume declines mainly in Latin America and Asia. Personal Health Care declined low single digits due to lower volumes as a result of a weaker cold and flu season, partially offset by higher pricing.

Fabric and Home Care organic sales increased 6% versus a year ago. Fabric Care increased mid-single digits due to increased pricing and a premium mix of fabric enhancers. Home Care increased high single digits due to increased pricing, favorable premium product mix, and volume growth.

Baby, Feminine, and Family Care organic sales increased 3% versus a year ago. Baby Care organic sales were unchanged. Feminine Care sales increased mid-single digits driven by increased pricing and favorable product mix, partially offset by volume declines in international markets. Family Care organic sales increased mid-single digits due to volume growth.

A Comment on Volumes

Not too long ago P&G had absolutely no volume growth, and each quarter seemed to be defined by 10% price increases and 4% volume declines, or something of the like. This is completely reversing each and every quarter, and we are now finally seeing volume growth in key markets. Over the past five quarters in North America volumes have been as follows: -3%, flat, +2%, +3%, and +4%. Europe is now moving to volume growth as well. If it weren’t for China P&G would have impressive total volume growth, a thought that seemed impossible just a few quarters ago.

Not only are we seeing volumes grow, they are accelerating. Volume growth is the healthiest form of growth for a packaged good company like P&G, and we are returning to volume growth being an important part of the overall growth story. This was pretty easy to predict when volumes were dropping like a rock, just due to comparisons in earnings and the essential nature of P&G’s products, and we are finally seeing it come to light.

P&G Using AI?

Talking about a company who sells diapers and dish soap using AI is a little funny to me, but there’s a story here. From the earnings call:

We're also using AI tools to optimize fill rates and for dynamic routing and sourcing optimization, $200 million to $300 million of savings opportunity across these areas. We have line of sight to savings from improved marketing productivity, more efficiency and greater effectiveness, avoiding excess frequency and reducing waste while increasing reach.

I don’t think it is irrational to belief P&G will be able to leverage AI to save hundreds of millions across all aspects of their business. If we are already seeing $200 to $300 million of savings because of AI, it is only going to get better. Using AI to increase advertising efficiency, drive supply chain continuity, and reduce waste in operations will greatly benefit P&G as this technology develops.

The productivity savings from AI are something I am going to monitor with P&G, and I wish I was an analyst on the call to ask this question every quarter. Productivity savings are straight margin growers, and this obviously has a trickle-down positive effect on the P&L.

If you told me just a year ago I would be talking about AI in an article about P&G, I’d call you crazy. But we now live in a world where even P&G needs to find ways to use AI to save on the bottom line, and it is currently working.

My Thoughts

Over the past two years I have been pounding the table on my outlook for P&G. I saw the margin expansion, earnings growth, and return to volume growth coming long before it became consensus. I refuted numerous analyst downgrades, which argued margins were going to be long-term compressed, and volume growth wasn’t returning anytime soon. I feel justified after this report, justified because I got the story right, and “professionals” didn’t.

Turning to the outlook for P&G itself, things couldn’t look much better. A return to a balanced mix of growth led by volume, continued growth in market and value share, and a stronger than ever portfolio. A major bearish thesis against P&G was that if we had a recession consumers would trade down and out of P&G products. This never happened, which is why volumes continue to grow in North America. P&G is seeing growth in their most premium product mixes, a sign that maybe the consumer isn’t slowing down like everyone expected. Even when consumers do trade down they have been trading down inside the P&G portfolio. When a product works, you don’t want to trade out of it. P&G products are just better, and people will pay for that.

5% top line growth. 8% earnings growth. 2.5% dividend yield. In theory this leads to an average return of 10.5% per year for investors in P&G. That is roughly the long run average for P&G, and is better than the S&P 500’s average return of 8% per year. Past results are not indicative of future returns, but P&G has a formula in place to steadily grow earnings and have an attractive shareholder return. Sure, it goes through time periods where it doesn’t move much, or where earnings have to catch up to its price, but with its strong brand portfolio and industry leading margins, it’s no wonder they’ve been around forever.

P&G is the largest holding in my portfolio. It has been for several years now. Each post-COVID quarter has gotten less and less exciting as business returns to normal, but it is great to see one of the world’s best companies be one of the world’s best companies.

Source: P&G Investor Relations.