3M and Kimberly-Clark Both Trade Lower After Mixed Earnings Reports

3M and Kimberly-Clark Both Trade Lower After Mixed Earnings Reports

3M and Kimberly-Clark both offer uninspiring guidance for 2024.

At the time of writing this article I own shares of KMB. This is not financial advice and is meant for entertainment purposes only.

Scheduling Update:

My article discussing Procter & Gamble’s earnings report will be this week’s Sunday newsletter. Kenvue, which would be the 4th and final company I report regularly report on, will be Sunday, February 11th’s newsletter.

Today’s Thursday edition of The Simple Stock Report discusses 3M and Kimberly-Clark, so buckle in we got a long one!

3M Earnings and (Potential) Improvement

3M has been an absolute mess over the past two years. Constant earnings misses, weak guidance, poor execution, serious pressure due to their PFAS and Combat Arms lawsuits, restructuring, and terrible share price performance. During this time, I have been VERY bearish 3M, even calling the stock “uninvestable” on occasions, and I believe for good reason.

With that said, 3M MIGHT be turning a corner. I see potential for this company to go from “utterly hopeless” to “simply miserable” in the near future. So I’ll review the earnings and some executive commentary, then discuss my new thoughts on 3M.

We initiated actions to restructure our organization and simplify our supply chain, while progressing our Health Care spin and addressing legal matters. - 3M CEO Mike Roman

3M reported the following:

Net Sales of $7.7 billion, mostly in line with expectations.

EPS of $2.42, beating expectations of $2.31.

3M’s EPS of $2.42 was adjusted to remove one-time charges involving costs for litigation and other items, such as restructuring charges. This number increased 11% year-over-year from $2.18 despite absolutely no help from Net Sales, which were down -3% for the year total and -0.3% for the quarter. A large portion of this higher EPS was a roughly $500 million decrease in selling, general, and administrative costs. SG&A is much higher on the year as compared to last due to litigation costs, but this quarter saw a significant drop, which helped EPS.

3M’s fiscal year 2024 guidance was not at all inspiring, and was why the stock fell over 11% on Tuesday. They see total sales growth in a range of 0.25% to 2.25% (which is the first time I have ever seen .25%s used in a guidance range), EPS in a range of $9.35 to $9.75, and operating cash flow of $6.5 to $7.1 billion ($6.68 billion in operating cash flow in 2023). Nothing to write home about, but at least growth isn’t negative (for now).

One issue 3M shareholders should currently have is dilution. It is no secret companies issue new shares to pay employees who have these stock options and such, but often they will buy back more shares than they issue to prevent shareholder dilution. 3M has not been buying back shares of their stock recently because paying the dividend and debt has become enough of an issue (in my opinion), so shares outstanding are up to 555.4 million from 552.9 million last year. Not a huge increase here, but worth noting.

On the topic of cash flows, while they were much better than in 2022, the bar was low for improvement. They did see free cash flow increase 30% in 2023, which allowed them to reduce net debt by $2 billion (representing 17% of net debt outstanding), and pay $3.3 billion in dividends.

3M will be spinning off its health care segment into its own public company, and I am semi-convinced this is to have extra liquidity to pay off their settlements. From the earnings call:

Absent the proceeds from the intended spin-off of the Health Care business, the company has not concluded how it would fund amounts due under the Public Water Supplier and Combat Arms Earplug legal settlements. Therefore, we have not included the potential impacts of changes in net debt that may be needed to fund amounts under these agreements.

For illustrative purposes only, in the absence of the proceeds from the Spin, the adjusted earnings per share impact from financing the legal settlements could be up to approximately a $0.20 per share headwind,based on current market conditions.

So while they kind of say the opposite of what I believe, they do mention potentially using debt to fund the amounts they have to pay under these agreements. This would end up having a trickle down effect for 3M, hurting R&D spending which hurts growth, which hurts earnings, which hurts the dividend, and so on.

They do discuss their restructuring is going well with $400 million in savings throughout the organization. They’ve cut management layers, modernized technology, reduced worldwide real estate, simplified supply chains, and freed up resources to prioritize new growth areas. Only time will tell if this will actually work, but it seems to be a promising step in the right direction.

I am in the belief 3M needs a “reset” quarter. If they came out tomorrow and cut the dividend 50% I would be sold on the turnaround. This would free up significant cash to pay down debt, pay lawsuit settlements, and invest back into the business. I know this is the last thing management wants to do, as much of their shareholder base is in the stock for the income, but I would view this as a positive, and would look to become an owner at that point.

No, I don’t own 3M stock, and yes I have been very, very critical of them for over a year now. I am shifting my tone here from “I don’t trust you one bit” to “Okay maybe, but prove it”. I want 3M to prove to me it has some form of value. If it can find a way to get these lawsuits behind them and have the opportunity to focus on innovating in all aspects of science again I am all on board. Until then I’ll watch from the sidelines, with a slight belief in them being able to pull it off.

Kimberly-Clark Earnings

I will *attempt* to keep KMB’s report brief, so here goes nothing!

We enter 2024 having advanced the Company's strategic foundation and financial position, and with confidence this phase of cost recovery and supply chain stabilization is largely behind us. Moving forward, we will continue to invest in differentiating our brands and enhancing our capabilities while we maintain a disciplined cost structure in our next phase of growth. I'm confident we are positioned to accelerate and enhance the performance of our business and create meaningful shareholder value as we deliver our purpose of better care for a better world. - CEO Mike Hsu

Kimberly-Clark reported the following for Q4 2023:

Net Sales of $5 billion, in line with expectations and previous year’s earnings.

EPS of $1.51, below the $1.54 expected, down -2% from previous year’s earnings.

The Personal Care segment saw sales of $2.6 billion, up 2% in the quarter, +6% on an organic basis led by price, mix, and volume. Volume growth continued in North America, with volumes up 4%.

The Consumer Tissue segment saw sales of $1.5 billion, down -1% in the quarter and in line on an organic basis. Price gains of 1% were offset by volume declines of -1%. North American volumes increased quarter-over-quarter with volumes up 2%.

The KC-Professional segment saw sales of $816 million, down -3% on the quarter and down -1% on an organic basis. Improved pricing and mix were slightly offset by lower volumes.

Volumes are a major part of the story for companies such as Kimberly-Clark, so to see continued improvement in volumes is a promising sign to investors. Just a few quarters ago analysts doubted the ability of KMB to turn pricing growth into volume growth, but we are slowly starting to see the transition.

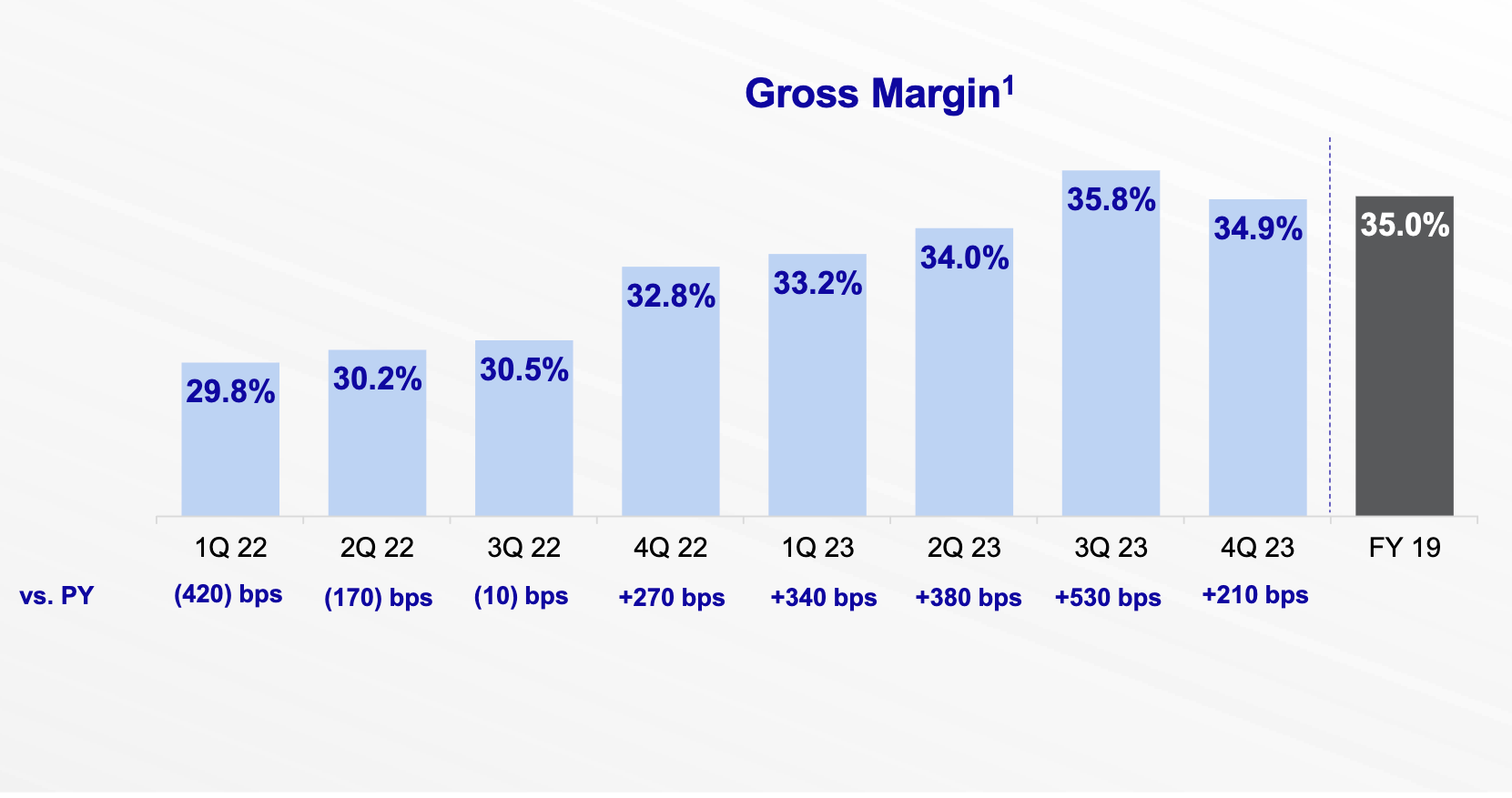

Margin recovery has been probably the most important story for Kimberly-Clark since the pandemic, and there is good news to report here. Gross margins improved 210 basis points to 34.9% in the quarter, which are now in line with pre-pandemic margins. Operating profit margins were lower at 13.5% for the quarter but still up 150 basis points on the year. Q4 operating margins were hurt by foreign currency exchange issues.

Management offered the following guidance for fiscal 2024:

The company currently expects to deliver a low-to-mid single digit percentage increase in 2024 Organic Net Sales versus the prior year period, with growth in reported Net Sales forecast to reflect negative impacts of approximately 300 basis points from currency translation and 60 basis points from the Brazil Tissue divestiture. Adjusted Operating Profit is expected to grow at a high single-digit to low double-digit rate on a constant-currency basis and Adjusted Earnings Per share are expected to grow at a high single-digit rate on a constant-currency basis versus the prior year period. Reported growth in Operating Profit and Earnings Per Share are currently expected to be negatively impacted by approximately 400 basis points from currency translation.

KMB shares fell well over 5% on Wednesday after they reported earnings, likely due to the uninspiring top-line sales growth guidance for 2024. KMB does a lot of business in foreign and developing markets, and have been absolutely crushed by foreign currency volatility in the past several years. They unfortunately see this continuing into 2024, as shown in their weak outlook.

The image below is one of my favorite things Kimberly-Clark does. It shows its outlook for the year in January 2023, then updated in October 2023, and then the real results. There’s a lot to takeaway from this, and I encourage you to look through, but I want to highlight two points here.

Share repurchases were $100 million higher than midpoint of guidance range. Management bought back a TON of stock in Q4, which means they must believe, as I do, that shares are undervalued.

Capital expenditures were lower than guided for. This helped to increase free cash flow, which lead to Kimberly-Clark reducing its net debt from $8.4 billion to $8 billion, repurchase the before mentioned shares, and increase its dividend 3.4%.

I, unfortunately, bought some KMB before earnings, and also after they reported and opened lower. That being said, I have never been more confident in Kimberly-Clark, and believe their business is in a strong place. With gross margins back to pre-pandemic levels, I believe they will only expand from here, a prospect that excites me.

Kimberly-Clark is an incredibly boring company (with an entertaining CEO to listen to on the conference call), but sell essential products. In the long term Kimberly-Clark’s value proposition to shareholders is low to mid single digit revenue growth, mid to high single digit earnings growth, which leads to an increasing dividend, decreasing shares outstanding, and paying off of debt. This quarter, more than anything, tells me they are ready for the post-pandemic, post-supply chain shock wave of business, and are becoming a more efficient company as each day passes.